The emerging market asset class is too broad, inhibiting investors from allocating capital to markets with promising growth opportunities.

The emerging market asset class is too broad, inhibiting investors from allocating capital to markets with promising growth opportunities.

2022 has proven an adage that has underpinned the global capital markets for decades: when developed markets cough, emerging markets catch the flu. Emerging markets (EMs) have faced a painfully slow recovery from the COVID-19 pandemic. Shocks to energy and food supplies exacerbated by the Russian invasion of Ukraine have intensified inflationary pressures and humanitarian concerns across many EM countries.

Monetary policy tightening by the Federal Reserve has led to depreciating currencies, higher borrowing costs, and dramatic capital outflows. All told, $38.5 billion flowed out of EM stocks and bonds in the first five months of 2022—the highest clip since 2005. With the global economy in a precarious position, investors have opted to shift their portfolios away from assets that are commonly perceived to entail more risk—EM assets being chief among them.

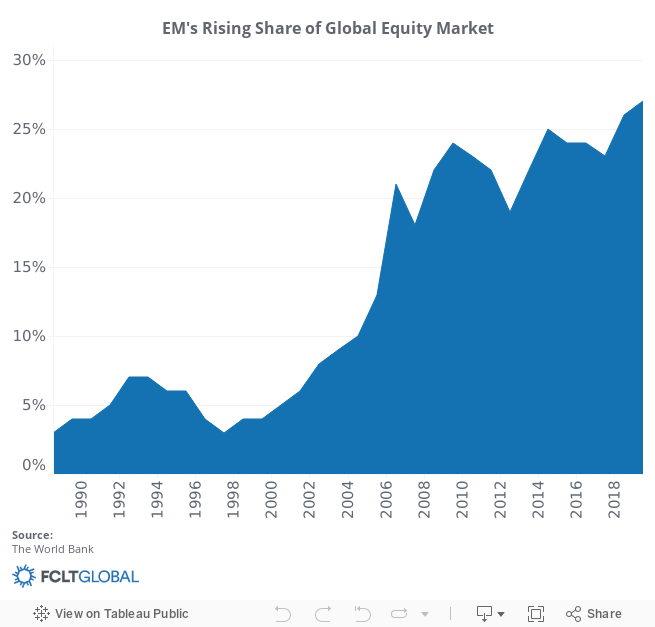

EMs encompass a richly diverse range of countries and companies that have unique risk and return profiles. Plus, EMs are significantly underweighted in global portfolios relative to their weight in global market capitalizations and their share of the global economy. Unfortunately, lumping all EMs together into one broad category blurs investors’ visibility into the long-term risks and opportunities of individual EMs.

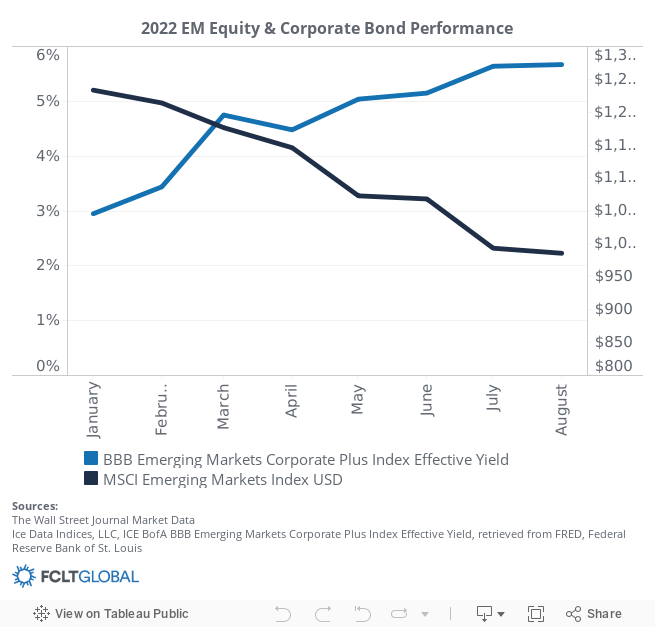

To illustrate this point, the MSCI Emerging Markets Index has fallen 23.8%1 since the beginning of the year. According to data from Refinitiv, in the same period, Brazil’s BOVESPA Index has appreciated by 6.7% and Indonesia’s JKSE Index by 9.3%. While there is some credence to the notion that these two markets are enjoying a rally from the recent uptick in commodity prices, India’s BSE SENSEX Index, comprised of a multitude of industrial and information technology companies, is up 1.5% since the start of the year—a significant contrast to the S&P 500 which is down 18.2%.

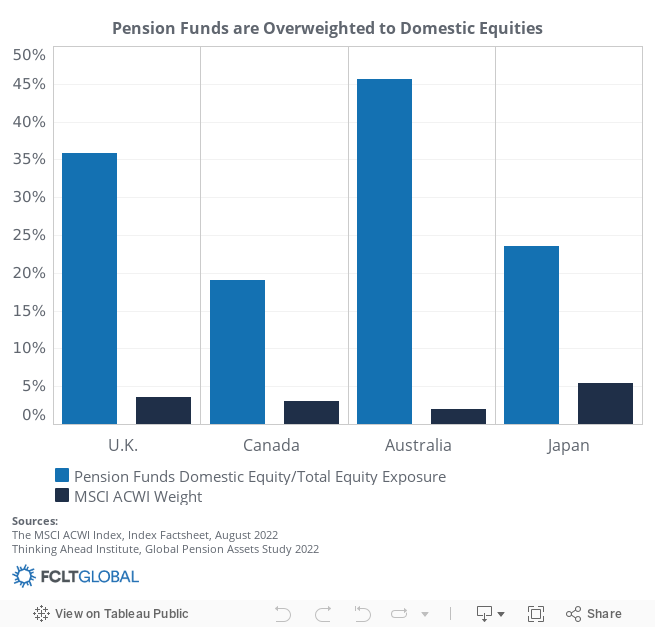

Most institutional investors—especially pension funds—tend to be drastically overweighted towards domestic equities. According to data from eVestment, the top 100 global equity funds have an average EM allocation of 6%. To put that figure in perspective, EM countries represent close to 35% of global GDP, listed EM companies represent about 26% of the global equity market cap, and although the MSCI ACWI is heavily weighted towards developed markets, EMs encompass 12% of the entire index.

While there are risks associated with investing in certain EMs—exchange rate fluctuations, relative illiquid capital markets, and regulatory risks— it would be short-sighted for investors to ignore the value certain EMs bring in terms of long-term growth potential and portfolio diversification. There is evidence to suggest that capital markets in EMs exhibit a low correlation with developed markets, which can reduce volatility across a balanced portfolio and generate steady returns for investors with long-term investment horizons.

As with any long-term investments, formulating a risk appetite statement can clarify an investor’s willingness and ability to prudently take risks and accept the uncertainties associated with portfolio allocations to EMs. Investing for the Future: A Long-Term Portfolio Guide provides a framework for institutional investors to improve the long-term outcomes of their portfolios. One of the key action areas of the framework entails developing such a risk appetite statement through the following processes:

In times of uncertainty, the temptation for investors to curtail their exposure to EMs is all too great. However, if investors disaggregate the EM asset class, utilize holistic benchmarks in their EM allocation strategies, and formulate clear risk appetite statements, they can capture long-term value-creating opportunities and support a more balanced and sustainable global economy.

As of 19 September 2022

Governance | Article, Toolkit

24 May 2022 - Geopolitical risk is currently front and center for executive management and boards. The war in Ukraine and accompanying geopolitical disruptions are an action-forcing event for nearly every multinational company and investor, regardless of the size of the business or portfolio at risk.

Investor Risk and Responsibilities | Report

21 December 2018 - Boards and executives of long-term funds, such as pension plans, sovereign wealth funds, and endowments, have a challenging problem. They need to manage those portfolios to meet their long-term purpose, which may be decades or more into the future. Yet no fund has the luxury of looking only to that long-term time horizon. Each must also meet expectations in the near term in order to continue in its role and with its investment strategy.

Report

23 March 2015 - In a recent survey of public and private pension plans and sovereign-wealth fund managers, respondents overwhelmingly agreed that while the ability to invest long term is an advantage, they do not necessarily have an effective set of implementation strategies/tools to help them realize their aspirations to be long term.