Most European executives are still paid on a 3-year basis, or less, data shows

Most European executives are still paid on a 3-year basis, or less, data shows

By Victoria Tellez and Sam Sterling

Some long-term investors are ready for companies to depart from the pay-for-performance status quo, but the jury is still out on the method that many of them are considering as a replacement.

Norges Bank Investment Management, the sovereign wealth fund that stewards Norway’s oil income, pioneered an alternative method that focuses on cultivating an ownership mindset and using time-centered share grants (i.e., long-duration). In its 2017 position paper, Norges emphasized that:

“A substantial proportion of total annual remuneration should be provided as shares that are locked in for at least five and preferably ten years, regardless of resignation or retirement. […] Allotted shares should not have performance conditions and the complex criteria that may or may not align with the company’s aims.”

Many investors around the world agreed. Indeed, this shift strongly implies long-term thinking, and investors are watching it closely to determine whether companies that use this approach outperform over the long term.

However, unsurprisingly, too few companies have used this plan for too little time to answer this long-term question empirically.

SEO Economics Amsterdam and Reward Value, a Netherlands-based nonprofit organization focused on executive compensation, illustrated these limits for us.

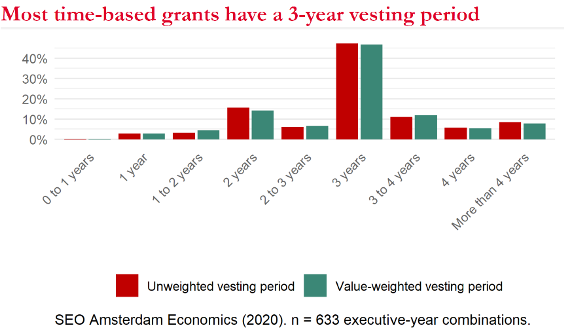

Vesting time-based stock grants after five or more years is still very uncommon. Specifically, less than 10% of time-based grants in SEO’s (European-only) dataset1 are longer than four years. While this data indicates that European companies are not yet meaningfully adopting this standard, they are still well ahead of US-based companies in this regard.

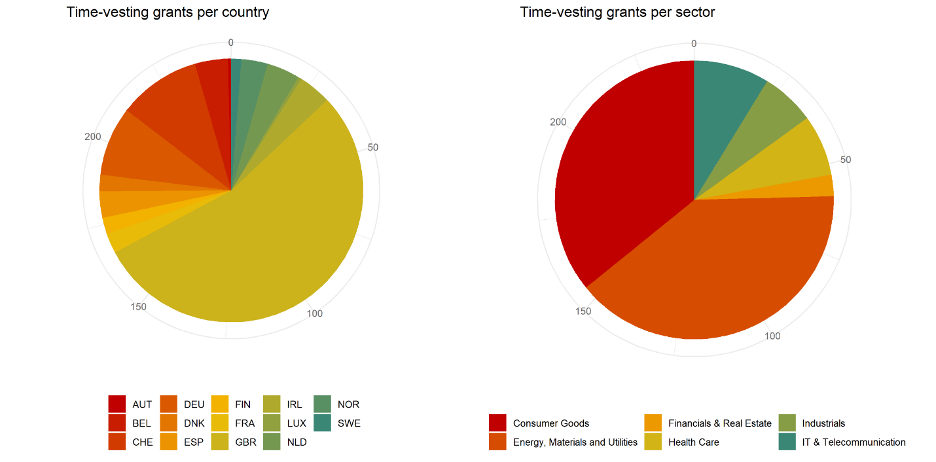

Additionally, about 50% of the sample is comprised of UK firms, and most firms are either in Consumer Goods or Energy, Materials, and Utilities sectors.

It is still too soon to tell what lasting effect Norges’ approach to executive pay will have on long-term corporate performance. In particular, more companies will need to experiment with this approach in order to draw long-term conclusions. In the interim, Norges’ transparent consideration of the pros and cons before arriving at an investment belief is unparalleled.

The lack of data does not prove or disprove the long-term validity of Norges’ proposed approach by any means. Rather, it just means that this approach reflects an investment belief right now, something with which long-term investors are very familiar and comfortable.

It also shows what it will take to reach an empirical conclusion: patience. Researchers cannot estimate long-term patterns without a long-term dataset. Accordingly, it will be some years before we can return to this question. In the meantime, if you have data relevant to this study, please contact FCLTGlobal’s research staff by emailing [email protected].

1. SEO’s dataset consists exclusively of European companies between 2009-2007. British firms account for about 50% of the European sample, and the Consumer Goods and Energy, Materials, Utilities sectors comprise about 75% of the European sample.

Incentive Alignment | Article

28 July 2020 - FCLTGlobal will research new ways in which short-term, status-quo compensation practices can be restructured to enhance long-term value creation.

In the News, Article

27 July 2020 - Rather than worrying about addressing near-term compensation shortfalls, compensation committees can use long-term incentives to keep executives focused on their business’ long-term strategy.

Metrics | Press Release

6 March 2020 - FCLTGlobal’s third Summit brings together top companies and investors