This report challenges the assumption that public markets are hostile to innovation, finding that companies with sustained R&D investment are more likely to survive and outperform over the long run — but that the payoff requires patience measured over years, not quarters. Innovation compounds over long time horizons while market pressures operate on short ones, and closing that gap demands deliberate action from CEOs and boards on governance, incentives, and investor engagement.

Public markets are often criticized for rewarding short-term performance over long-term innovation. Quarterly reporting cycles, activist pressure, and earnings expectations can make sustained investment in research and development feel increasingly difficult to justify, especially when the payoff may take years to materialize.

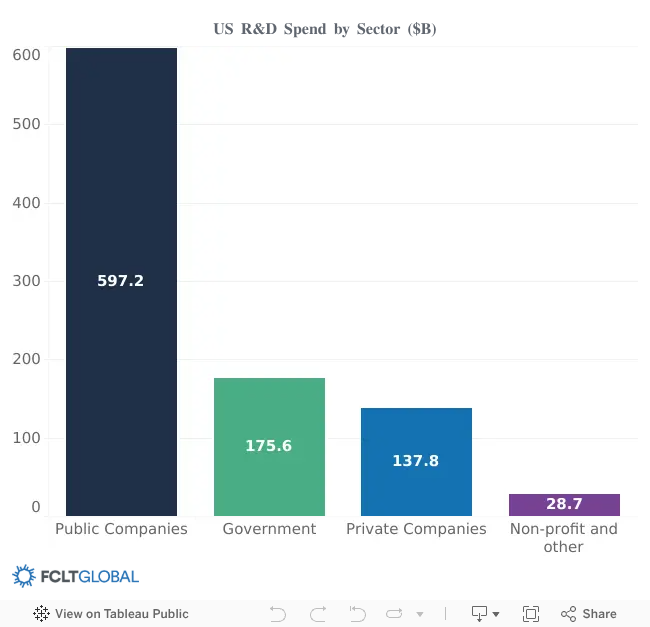

Yet despite those pressures, public companies remain the world’s dominant engine of innovation spending. In the United States alone, public companies account for roughly two-thirds of total R&D investment, outspending private companies, government, and nonprofits combined. From AI infrastructure to biotechnology breakthroughs, many of today’s most significant innovations are emerging from or alongside public companies.

var divElement = document.getElementById(‘viz1784638916337’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; if ( divElement.offsetWidth > 800 ) { vizElement.style.width=’650px’;vizElement.style.height=’627px’;} else if ( divElement.offsetWidth > 500 ) { vizElement.style.width=’650px’;vizElement.style.height=’627px’;} else { vizElement.style.width=’100%’;vizElement.style.height=’727px’;} var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

This report examines a central question: Do public markets actually reward sustained investment in innovation over the long term?

Drawing on MSCI ACWI data from 2009–2024, the analysis compares companies based on R&D intensity relative to sector and regional peers. The findings suggest that while the market may not reward innovation immediately, companies that sustain higher levels of R&D investment are ultimately more likely to survive and outperform over long horizons.

Key Findings:

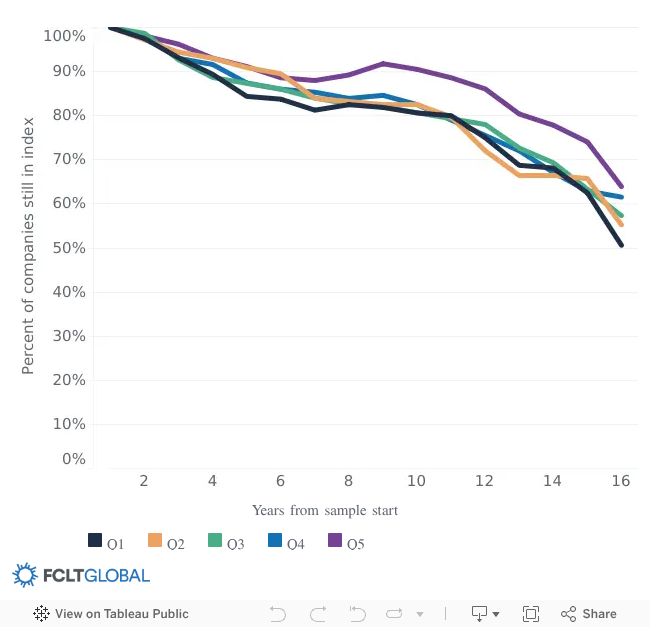

R&D Intensive Firms Survive Longer

Companies with the highest R&D intensity were 13 percentage points more likely to remain in the MSCI ACWI over the study period than those with the lowest.

var divElement = document.getElementById(‘viz1784639034041’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; if ( divElement.offsetWidth > 800 ) { vizElement.style.width=’650px’;vizElement.style.height=’627px’;} else if ( divElement.offsetWidth > 500 ) { vizElement.style.width=’650px’;vizElement.style.height=’627px’;} else { vizElement.style.width=’100%’;vizElement.style.height=’727px’;} var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

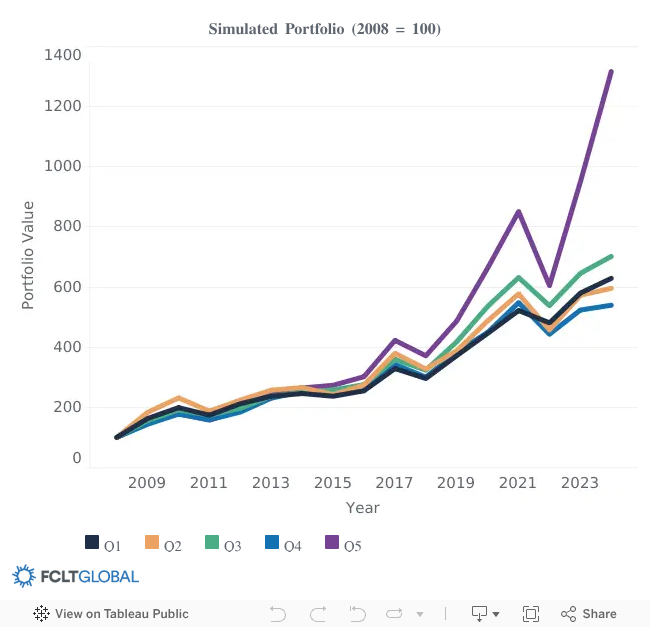

R&D Intensive Firms Outperform in the Long Run

High-R&D firms outperformed low-R&D peers by roughly 5 percent annualized over a 15-year period. However, that performance gap did not become meaningfully visible until approximately year eight.

var divElement = document.getElementById(‘viz1784639443637’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; if ( divElement.offsetWidth > 800 ) { vizElement.style.width=’650px’;vizElement.style.height=’627px’;} else if ( divElement.offsetWidth > 500 ) { vizElement.style.width=’650px’;vizElement.style.height=’627px’;} else { vizElement.style.width=’100%’;vizElement.style.height=’727px’;} var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

The report also challenges several common assumptions about innovation in public markets, including the belief that public companies cannot produce breakthrough innovation, that private markets inherently innovate faster, or that heavy R&D spending weakens long-term survivability.

For CEOs and boards, the findings point to a broader challenge: balancing near-term market scrutiny with the long-term investment horizons required for transformational innovation. Companies that succeed tend to combine sustained R&D investment with corresponding incentives, clear communication around long-term strategy, and shareholder engagement built around that strategy rather than short-term predictability.

Ultimately, the report concludes that innovation is not absent from public markets — it is often simply that traditional accounting metrics don’t always capture the efficiency or value creation potential of innovation.

5 March 2026 - On 25 February 2026, we had the privilege of bringing together our members and other leaders in global business and investing for FCLT Summit 2026, FCLTGlobal’s annual convening, where we address the most pressing challenges facing long-term value creation in today’s capital markets.

27 January 2025 - On 21 January, FCLTGlobal convened its annual Davos CEO Roundtable for leaders from across industries to discuss how Europe has real opportunities for appreciation if policymakers can unleash its strengths.

9 August 2020 - R&D spending, especially long-horizon R&D project spending, faces a unique set of short-term pressures relative to other types of long-term investment. When facing short-term financial pressures, behavioral biases including manager risk aversion and uncertainty around forecasting potential future returns (among other things) lead to a tendency among management teams to cut long-horizon projects first. The declining tenure of managers, the lack of innovation-linked metrics in incentive compensation plans, the typically asymmetric return profile of long-horizon projects, and an investment community that often ignores the potential impact of long-horizon innovation spending in a company’s valuation analysis all contribute to this...