Sovereign wealth funds (SWFs) are rapidly emerging as the world’s dominant long-term investors.

Sovereign wealth funds (SWFs) are rapidly emerging as the world’s dominant long-term investors.

Over the past 15 years, their assets under management have nearly tripled.1 Along with this increase, their investment behavior is shifting just as dramatically. According to our latest FCLT Compass report, based on a data set measuring global investment horizons and capital flows since 2009, SWFs’ average allocation to private market assets has climbed from just 3 percent in 2009 to 33 percent in 2024. Several of the largest funds now allocate more than half their portfolios to these long-horizon, illiquid assets, all at a scale unmatched by any other institutional investor.

This evolution positions SWFs as the new drivers of long-term capital. As defined benefit pensions recede and individual retirement plans emphasize liquidity, sovereign wealth funds – state-backed, structurally patient, with investment horizons spanning decades – are now companies’ long-term owners.

The scale and structure of SWFs make them uniquely suited to serve as drivers of long-term capital. Several of the world’s largest, including NBIM, CIC, GIC, and ADIA, were built explicitly to invest for their countries’ future generations. Backed by foreign exchange surpluses or resource revenues, and largely unconstrained by near-term liabilities, they are free to pursue multidecade mandates.

Their size further amplifies this advantage. With hundreds of billions of dollars under management, leading SWFs can underwrite massive projects and absorb short-term market volatility. Unlike banks, which must maintain liquidity, or insurers, which must match near-term liabilities, SWFs can hold illiquid investments through full economic cycles. Long-term-oriented endowments and foundations share similar orientations, but at a fraction of their size.

The scale and structure of SWFs make them uniquely suited to serve as long-term capital stewards2

| Fund | Country | AUM ($Billions) |

|---|---|---|

| Norges | Norway | 1,548 |

| CIC | China | 1,240 |

| SAFE | China | 1,076 |

| ADIA | United Arab Emirates | 968 |

| KIA | Kuwait | 846 |

| GIC | Singapore | 769 |

| Public Investment Fund | Saudi Arabia | 764 |

| Qatar Investment Authority | Qatar | 510 |

| ICD | United Arab Emirates | 341 |

| Temasek | Singapore | 288 |

| Mubadala | United Arab Emirates | 276 |

| ADQ | United Arab Emirates | 196 |

| Turkey Wealth Fund | Turkey | 190 |

| Korea Investment Corporation | South Korea | 189 |

| Future Fund | Australia | 186 |

Crucially, SWFs are not just passively patient; they are actively increasing their exposure to long-horizon investments. SWFs in emerging markets have more than doubled their assets under management in the past decade, with nearly half of new capital deployed into private markets – an arena once dominated by pension plans.

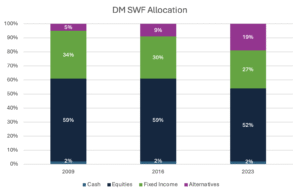

Figure 1: The Quiet Shift: SWFs Reweight Toward Illiquid, Long-Horizon Assets

As shown in Figure 1, sovereign wealth funds have dramatically increased their exposure to private markets over the past 15 years. In 2009, private assets represented only about three percent of the average SWF portfolio. By 2024, that share had jumped to roughly one-third of assets. Some of the largest SWFs now allocate more than 50 percent of their portfolios to illiquid assets such as private equity and infrastructure – a level of long-horizon commitment unmatched by pension funds or insurers.

Across infrastructure, energy, technology, and logistics, SWFs are backing projects whose value may take years or decades to unlock. As other institutional investors lose their capacity to hold long-horizon assets, SWFs are moving to fill the void in long-term capital.

For decades, defined benefit (DB) pensions served as the financial system’s primary source of long-term capital. With predictable outflows and large asset pools, they could allocate meaningfully to illiquid assets in pursuit of stable, long-run returns. Some even rivaled SWFs in size and risk appetite.

That model, however, is now in decline. Across developed markets, from the U.S. and U.K. to Australia, Canada, and the Netherlands, corporate and public DB pensions have been steadily replaced by defined contribution (DC) plans. With the exception of the Australian superannuation system, most DC plans are individual accounts, such as 401(k)s, shifting investment decisions from institutional investors to households. Unsurprisingly, households tend to favor liquidity, simplicity, and low fees.

Until very recently, most DC plans excluded private market investments entirely, and it’s only in the past year that the US began formally considering private equity in 401(k) plans. While markets like Australia have developed more robust private market participation, the structural tilt of most DC plans remains toward public markets and daily-priced funds.

Meanwhile, many remaining DB plans have shifted toward more liquid assets to manage near-term liabilities. Combined, these forces have led to a clear pullback from long-horizon investing by traditional pensions.

This raises a critical question: as pensions step back, who will fund long-term opportunities going forward?

So far, sovereign wealth funds have stepped into this gap. Leading funds in the Middle East and Asia-Pacific, in particular, are backing long-term development projects with confidence. Across energy transition, logistics infrastructure, and innovation hubs, these funds are backing initiatives that take years to unfold. When short-term investors retreat, SWFs increasingly act as anchor investors, providing stability and capital continuity.

Their role isn’t just financial. Many sovereign wealth funds deliberately align national priorities with investment mandates, supporting domestic development, economic diversification, or strategic industries, while continuing to pursue long-term returns. The result is a rare combination of scale, patience, and alignment. In an increasingly fragmented investment landscape, that combination is proving powerful.

As investor horizons shorten and economic uncertainty mounts, sovereign wealth funds are playing a critical role in capital flows. They have both the mandate and the means to invest through cycles, take illiquidity risk, and underwrite future-focused projects.

The DB-to-DC transition is not going to reverse. Nor are the structural constraints of banks and insurers going away. That leaves sovereign wealth funds as one of the few actors with the capacity to think in decades rather than quarters.

1. Sarah Keohane Williamson, The CEO’s Guide to the Investment Galaxy (John Wiley & Sons, 2025).

2. Adapted from Sarah Keohane Williamson, The CEO’s Guide to the Investment Galaxy (John Wiley & Sons, 2025), 39, and Thinking Ahead Institute’s Asset Owner 100 (2024).

In the News

22 July 2024 - Sovereign wealth funds ensure that national wealth is preserved and utilized for the benefit of future generations, promoting sustainable economic development. Could the US benefit from a similar model?

Governance | Podcast

4 September 2024 - “Having a strong and clear foundation and clear governance around who can make decisions, then puts you in a very strong position for a volatile world.”

Governance | Article

15 July 2024 - On 25 June 2024, FCLTGlobal joined the International Forum of Sovereign Wealth Funds’ (IFSWF) Governance Workshop in London to lead a two-part discussion on avoiding short-term pressures and fostering a long-term investment ecosystem centered on meeting their citizens’ needs.