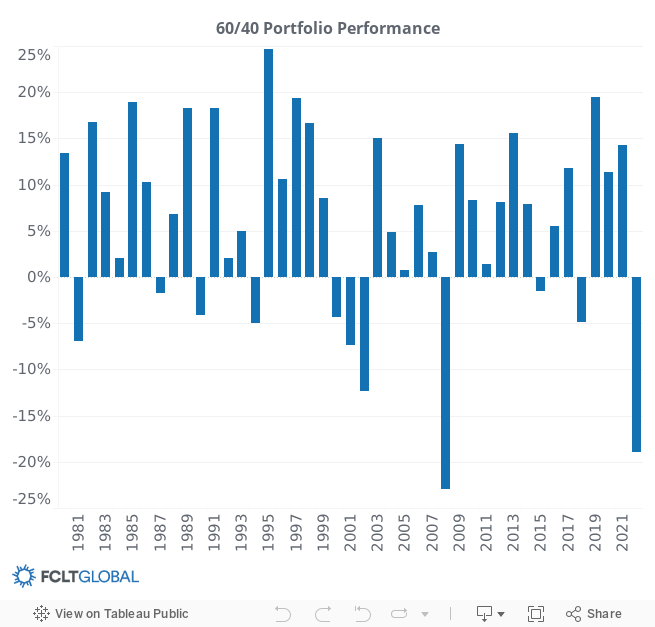

Recently, there have been a litany of pronouncements that the 60/40 portfolio is dead. This classic mix of 60% public equities and 40% fixed income has been a bellwether over time for asset allocators – as equities provide return and bonds balance equity risks.

As of the end of 2022, the traditional 60/40 portfolio has declined by 19%, the worst drawdown since the 2008 global financial crisis. The performance of this portfolio is a signal of how traditional equities and fixed income perform, and it’s a simple portfolio to construct.

As investors grapple with surging inflation, rising interest rates, turbulent geopolitics, and the mounting likelihood of recession, asset owners like pension funds, sovereign wealth funds, insurance companies, and endowments are facing significant uncertainties. While market participants begin to grasp the effects of elevated interest rates on the global economy, it is crucial to look back on the low-interest rate environment and gain a sense of how it has impacted the capital allocation decisions of institutional investors.

var divElement = document.getElementById(‘viz1675703548427’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; if ( divElement.offsetWidth > 800 ) { vizElement.style.width=’655px’;vizElement.style.height=’627px’;} else if ( divElement.offsetWidth > 500 ) { vizElement.style.width=’655px’;vizElement.style.height=’627px’;} else { vizElement.style.width=’100%’;vizElement.style.height=’527px’;} var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

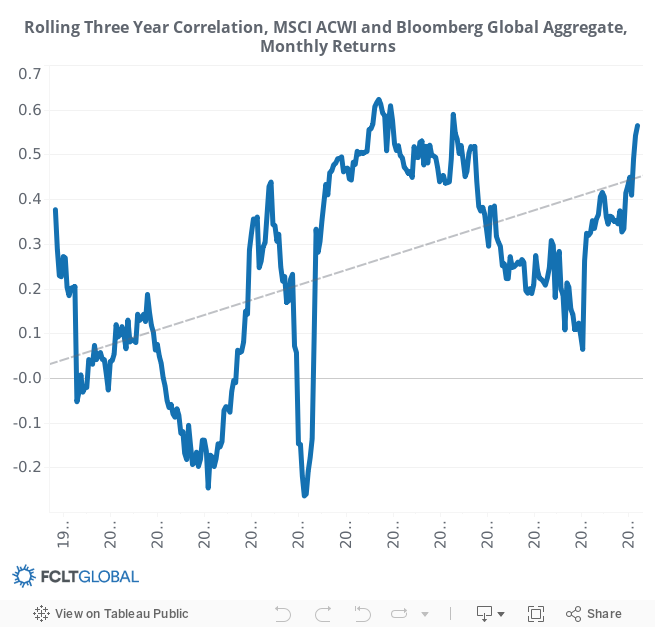

However, the era of low-interest rates has been the death knell for fixed income. Yields on bonds have been insufficient at generating returns for institutional investors, which has put pressure on the traditional 60/40 ratio. Global yields have been in secular decline for years, leaving less room for fixed income to outperform during periods of equity market volatility.

var divElement = document.getElementById(‘viz1675707366794’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; if ( divElement.offsetWidth > 800 ) { vizElement.style.width=’655px’;vizElement.style.height=’627px’;} else if ( divElement.offsetWidth > 500 ) { vizElement.style.width=’655px’;vizElement.style.height=’627px’;} else { vizElement.style.width=’100%’;vizElement.style.height=’527px’;} var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

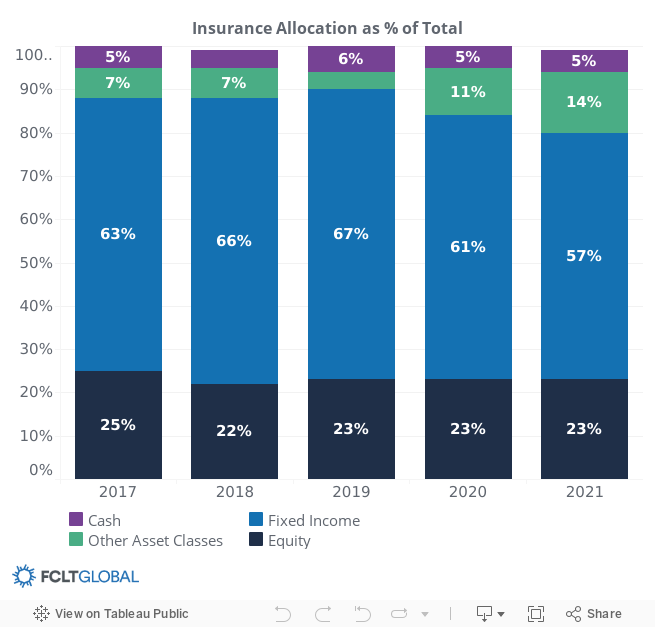

New data from FCLTCompass – a reporting of global investments and capital allocations – shows institutional investors have been increasing their investments in alternative assets. In fact, insurance companies – who typically invest large amounts in fixed income – have faced significant headwinds navigating the low-yield environment. The data shows allocations to other asset classes, including alternatives, have increased to 14% of total assets at the end of 2021, while fixed income has declined to 57%.

var divElement = document.getElementById(‘viz1675707516306’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; if ( divElement.offsetWidth > 800 ) { vizElement.style.width=’655px’;vizElement.style.height=’627px’;} else if ( divElement.offsetWidth > 500 ) { vizElement.style.width=’655px’;vizElement.style.height=’627px’;} else { vizElement.style.width=’100%’;vizElement.style.height=’527px’;} var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

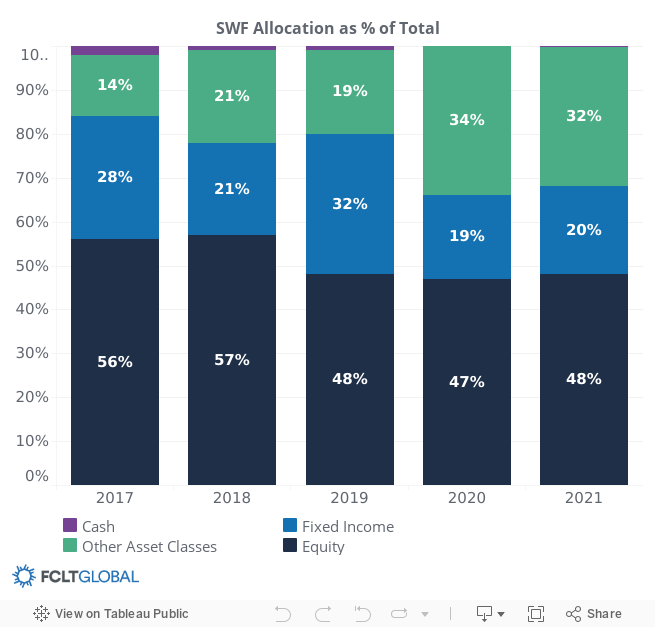

Moreover, sovereign wealth funds made significant increases to investments in other asset classes, from just 14% of total assets in 2017 to 32% in 2021, funded through a reduction in listed equities and fixed income.

var divElement = document.getElementById(‘viz1675707797854’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; if ( divElement.offsetWidth > 800 ) { vizElement.style.width=’655px’;vizElement.style.height=’627px’;} else if ( divElement.offsetWidth > 500 ) { vizElement.style.width=’655px’;vizElement.style.height=’627px’;} else { vizElement.style.width=’100%’;vizElement.style.height=’527px’;} var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

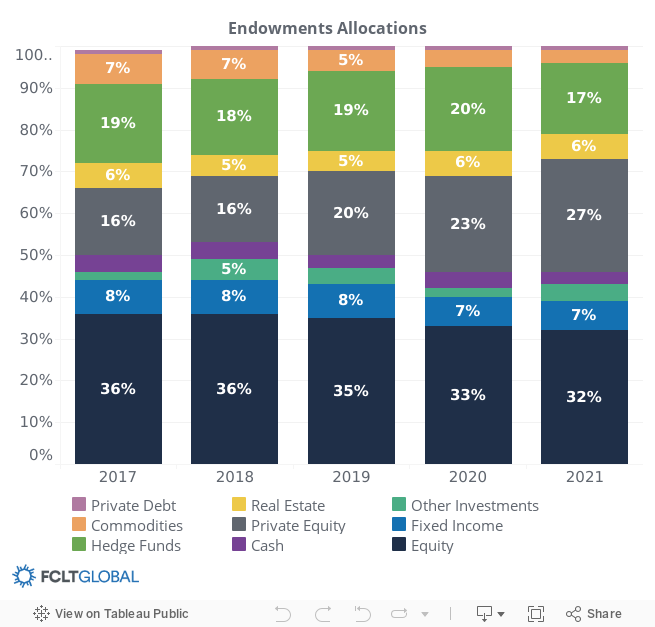

Much of the growth observed in other asset classes has been due to investments in illiquid markets such as private equity, real estate, and infrastructures. Endowments, for example, invested over 50% of total assets in alternative investments, with allocations to listed equities and fixed income shrinking over the past five years. On the other hand, private equity allocations grew significantly from 16% of total assets in 2017 to 27% in 2021.

var divElement = document.getElementById(‘viz1675707945845’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; if ( divElement.offsetWidth > 800 ) { vizElement.style.width=’655px’;vizElement.style.height=’627px’;} else if ( divElement.offsetWidth > 500 ) { vizElement.style.width=’655px’;vizElement.style.height=’627px’;} else { vizElement.style.width=’100%’;vizElement.style.height=’527px’;} var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

There are signs that the allure of alternative assets has begun to wane among institutional investors. Precipitous declines in the public markets have caused many investors to become overweighted toward private market assets, significantly curbing allocations to alternatives. For example, in the first half of 2022, global private equity fundraising shrunk by $122 billion compared to the same period in 2021. Additionally, as interest rates rise, there has been an increase in yields in global bond markets, which may resuscitate fixed income in the near future. All things considered, the 60/40 portfolio may make a comeback yet.

To learn more about these and other trends, watch our recent panel discussion, featuring experts from AIMCo, Liberty Mutual, and State Street Global Markets, about notable changes in capital allocation trends over the past year, how inflation has affected capital market behavior, and implications for both corporate and investor resilience in a recovering economy.

5 December 2022 - FCLTCompass is an annual benchmarking tool tracking long-term investment behavior on a global scale. The results of the latest analysis suggest that investment horizons receded in 2021 due to global disruptions such as inflation and COVID-19 recovery efforts.

7 December 2022 - This year's edition of FCLTCompass looks at the economics of recovery and observes how companies, investors, and national economies plan for a return to normalcy.