Data from FCLTCompass reveals short-term trends in the region

Data from FCLTCompass reveals short-term trends in the region

By Allen He and Ariel Babcock

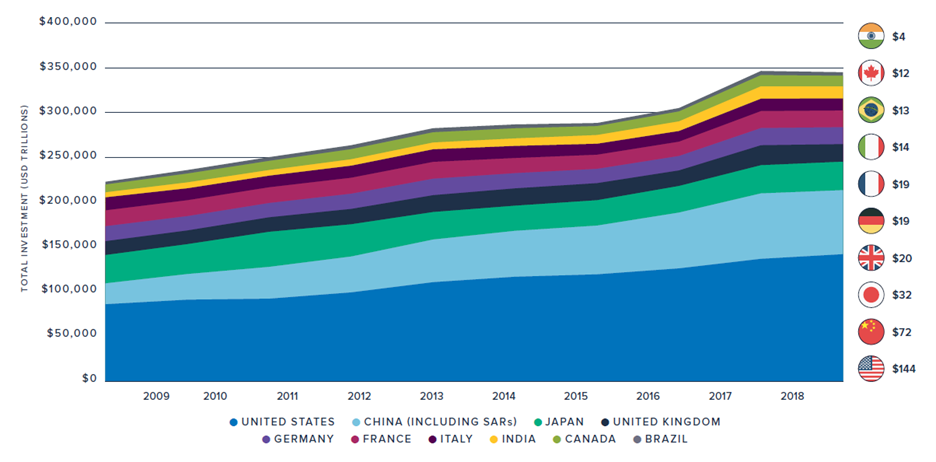

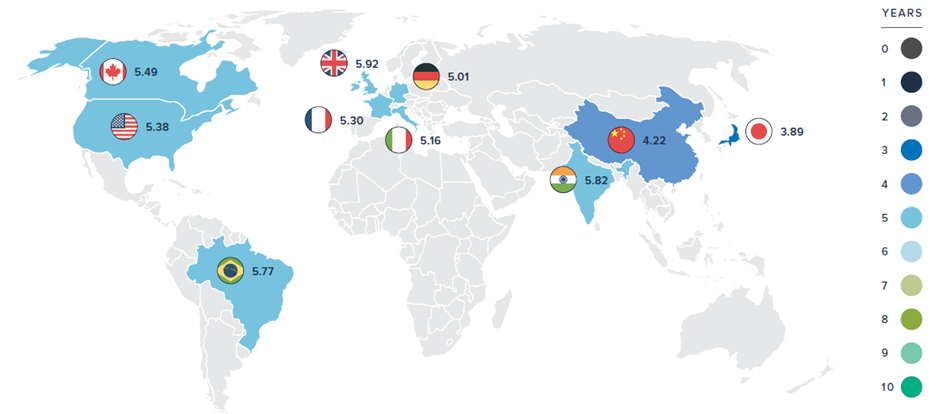

Wealth accumulation in China accelerated over the 10-year period from 2009-2018, giving China’s household savers increasing influence over global capital markets. Alongside this growth, data from FCLTCompass shows that savers in China (including special administrative regions of Hong Kong and Macau) have among the shortest-term allocations in the world, second only to their counterparts in Japan. Several factors influence this behavior, and there are several steps that could be taken to lengthen investment horizons in the region.

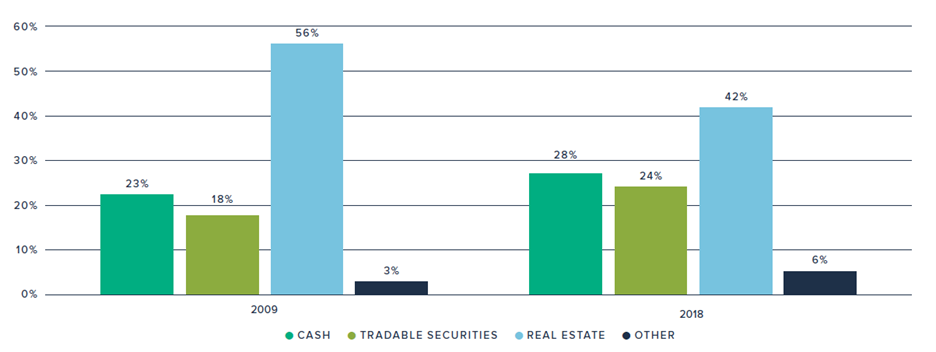

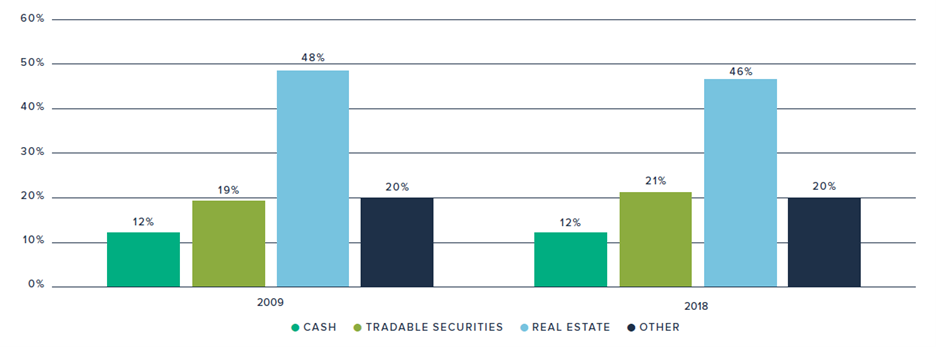

The shortening of savers’ time horizons in China (including SARs) is driven by higher portfolio allocations to cash and real estate versus other asset classes, a preference that has dominated that market since at least 2009. In particular, savers in China allocate to cash at roughly twice the rate of households elsewhere in the world. Several structural reasons account for this preference, namely that domestic equity markets are more volatile and less mature, making the risk-reward profile less attractive for conservative savers. Several sources have likened the Chinese stock market to a casino, and small investors have been on record saying that investing in equities “is just like gambling.”

What else might be contributing to a hesitancy among Chinese savers to diversify their asset allocation?

Although 96% of Chinese corporate credit was listed as investment-grade as recently as the end of 2019, those generous ratings have recently been called into question. Defaults are starting to rise, demonstrating that domestic credit ratings are not capturing the full picture and making savers less likely to deploy capital in fixed-income markets.

Additionally, alternative and emerging asset classes are still in early phases of maturity in the region. Although the Qualified Domestic Limited Partnership (QLDP) structure was first introduced by Chinese regulators in 2012 to facilitate renminbi investments into overseas funds, the licenses were heavily controlled with a quota scheme that limited access significantly. While quotas have been increased in recent years, they remain in place and serve to limit the flow of capital towards alternatives investments, especially overseas alternatives.

Furthermore, there remains a lack of broader access to investment products, which has skewed investor preferences. Retail investors account for 60% of the investable assets under management in China. Up until quite recently, those retail investors (classified as “Households” in the FCLTCompass dashboard) accessed investments primarily through local banking relationships. This limited the availability of investment products and may have contributed to the preference for real assets (e.g. real estate). Surveys also suggest a lack of financial literacy, which can contribute to a preference for conservative asset classes or those where there exists a principal guarantee.

What will it take to shift the balance toward more long-term assets? Mainly, access to more developed tradable securities markets (i.e., equity, debt, and derivatives markets) would allow savers to invest their cash in assets beyond real estate, as they do in other major economies around the world. More options would likely produce a new mentality with regard to savings, toward building future value and away from simply holding cash without the possibility for growth.

Given the status quo of Chinese markets, it is understandable why savers have concentrated their money so narrowly for so long, despite astronomic wealth growth. If that tendency shifts over time, the allocation behavior will carry significant implications for investment patterns in the region more broadly given the sheer scale of their collective capital, and asset class rotation will be necessary to ensure that households can achieve their long-term savings goals.

18 December 2024 - FCLT Compass is a dashboard measuring the investment horizons of the global investment value chain, how households are saving and allocating their money, and how long they can live off those savings. Calculating these metrics provides a holistic understanding of the long- or short-term orientation of global capital markets and how that orientation impacts the financial futures of millions of people worldwide.

Risk and Resilience | Article

25 January 2021 - In a decade-long low interest rate environment, riskier asset classes have seen accelerated asset gathering as savers chase yield.

Podcast

11 January 2021 - Our first episode of 2021 introduces FCLTCompass, our new dashboard tracking long-term investments on a global scale. Listen to a special replay of our launch event, held on 10 December 2020, to learn more about the dashboard and its important findings. For more information, click here. This episode is also available on Apple, Spotify, and YouTube. To learn more, visit the homepage for Going Long with FCLTGlobal.