What makes an investor quintessentially “long-term”?

What makes an investor quintessentially “long-term”?

What makes an investor quintessentially “long-term”? This question is at the core of FCLTGlobal’s mission and research agenda. Together with our partners at CEM Benchmarking Inc., we surveyed 18 large global asset owners responsible for a combined $1.6 Trillion in assets, about how they act to realize their long-term goals and what outcomes they’re seeing as a result. Our inspiration for probing these particular topics came from the 2015 Long-Term Portfolio Guide, published by the Focusing Capital on the Long Term initiative.

Although the survey size is small, it revealed several key traits of owners who, over a 10-year horizon, successfully added net value (after fees) relative to their own organizational benchmarks. Below is a further exploration of these traits and what they suggest it will take for an asset owner to truly achieve a comprehensive “long-term” approach to investment and value creation.

First, on average, the high-performing owners were larger: managing an average of $146 billion, compared to an average of $33.5 billion for the lower-performing owners. Larger owners have the scale to manage a larger proportion of assets internally and negotiate lower fees from asset managers, among other benefits, and this gives them an advantage when performance is measured net of fees.

Second, net-outflow funds in our survey were just as able to add ten-year net value as net-inflow funds. Funds in a net outflow position must maintain higher levels of liquidity and lower appetites for volatility, leading to the stereotype that investing for the long term is a luxury that they cannot afford. Five of the eight respondents in the high net value added (NVA) group were cash flow negative, suggesting that this stereotype isn’t necessarily accurate. This is encouraging. Retirees are growing as a share of the total population in many countries around the world, and outflows from their pension funds will increase accordingly. It still is possible for them to add value in the long term – and imperative that they do so for the future seniors who rely on them.

Several tenets of investment appeared consistently among the owners that we surveyed, as illustrated below

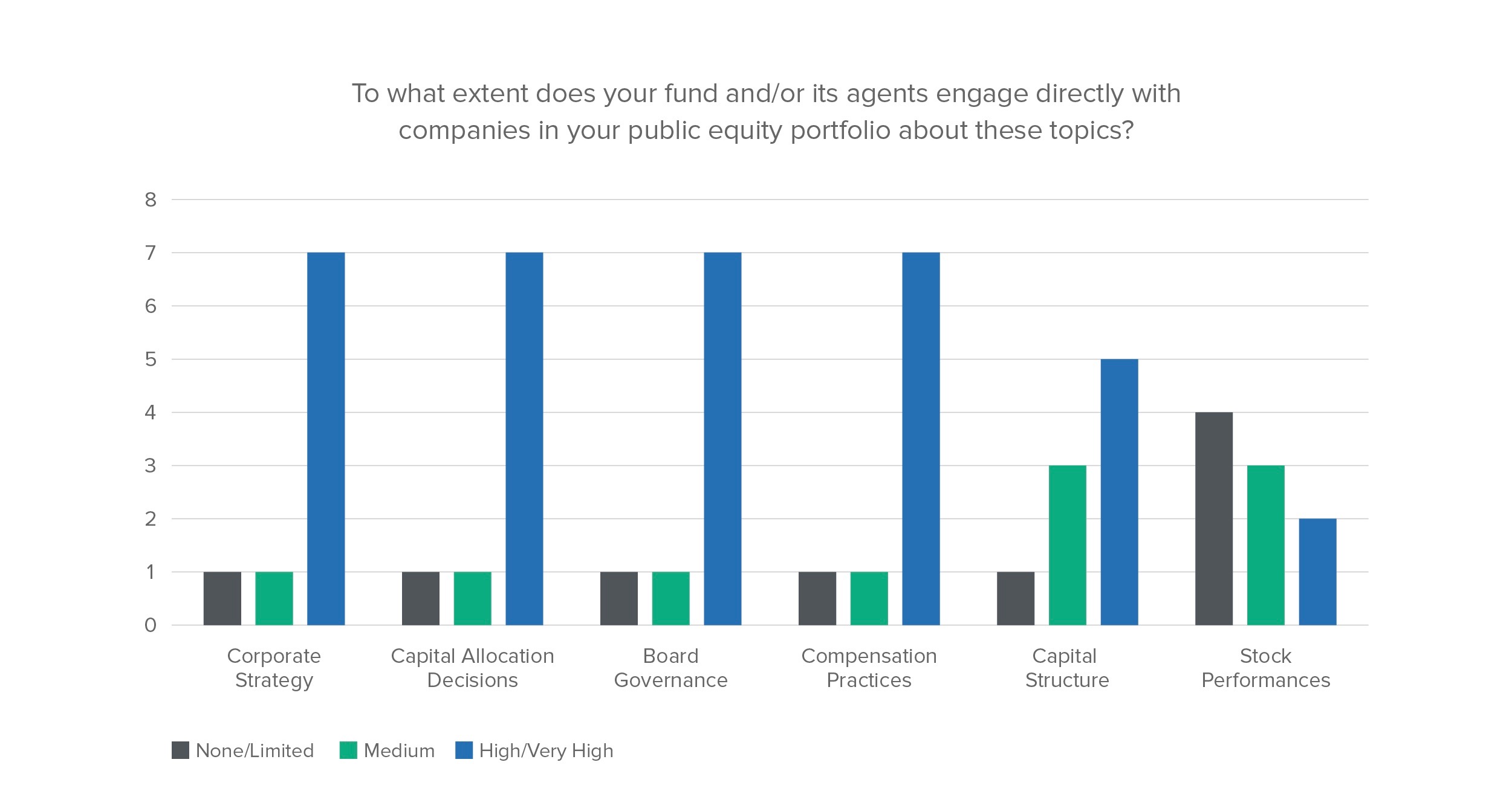

In engaging with companies in their stock portfolio, asset owners that added ten-year net value in our survey prioritized corporate strategy, capital allocation, board governance, and compensation practices in their engagement with companies in their stock portfolio. Most of them gave much less priority to the performance of the company’s stock. This corroborates recent FCLTGlobal research on the investor-corporate dialogue. “Long-term investors say they are less interested in quarterly results than in long-term business drivers,” we wrote in that study. “As one investor put it, ‘It’s all about the horizon. Long-term investors don’t need a lot of detailed guidance about quarterly numbers. They need clarity, consistency and transparency from managers in communicating strategic priorities and their long-term expectations’.”

Asset owners that added ten-year net value in our survey also tended to engage with corporate directors more than funds that were not able to create this long-term value. Five out of nine value-adding funds in our survey reported that directors were involved or very involved in their corporate engagements, compared to just three out of nine funds that were not able to add net value over ten years. We are encouraged that asset owners that tend to engage directly with corporate directors also tend to engage with them on the topics of corporate strategy and capital allocation.

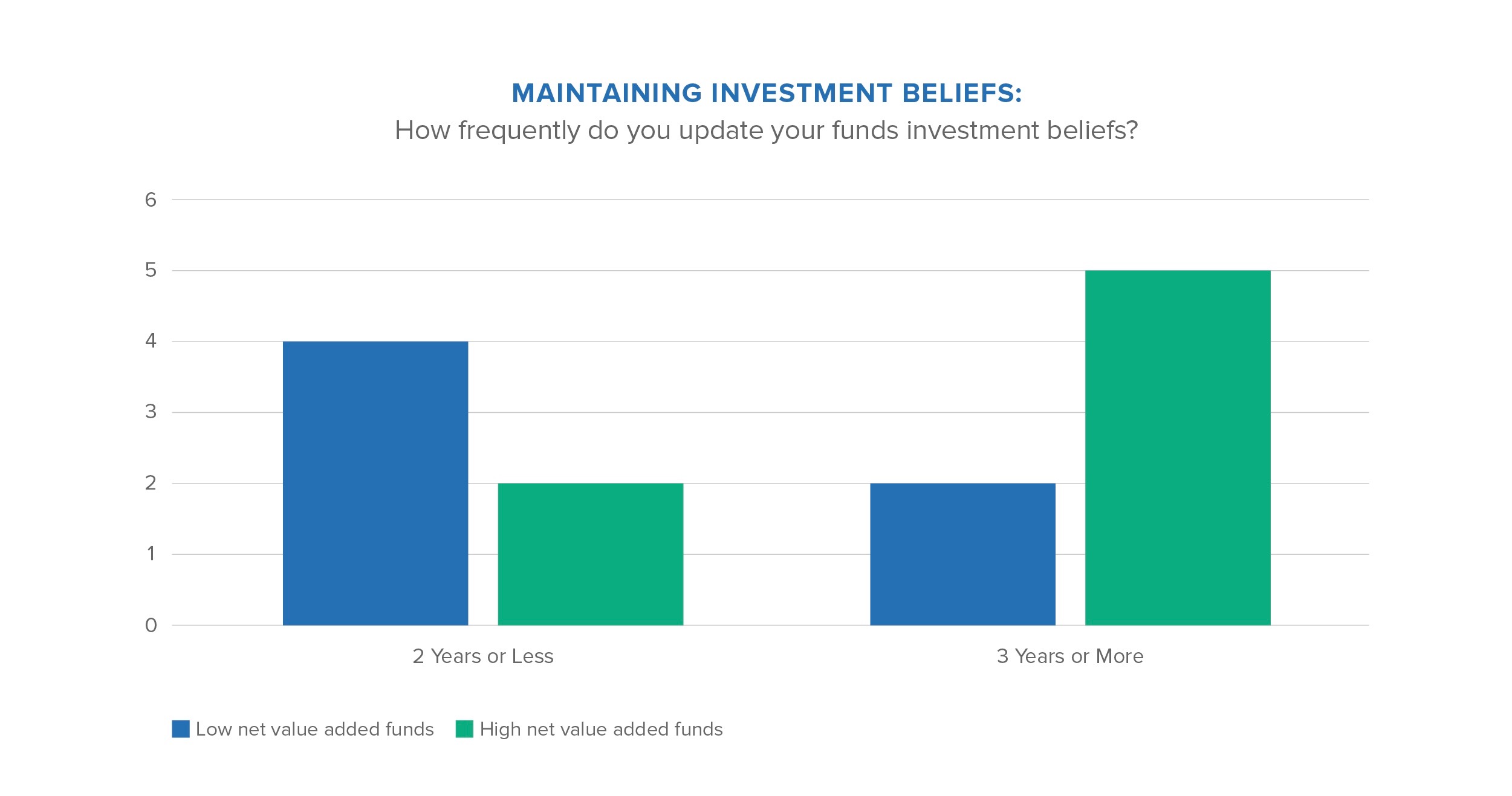

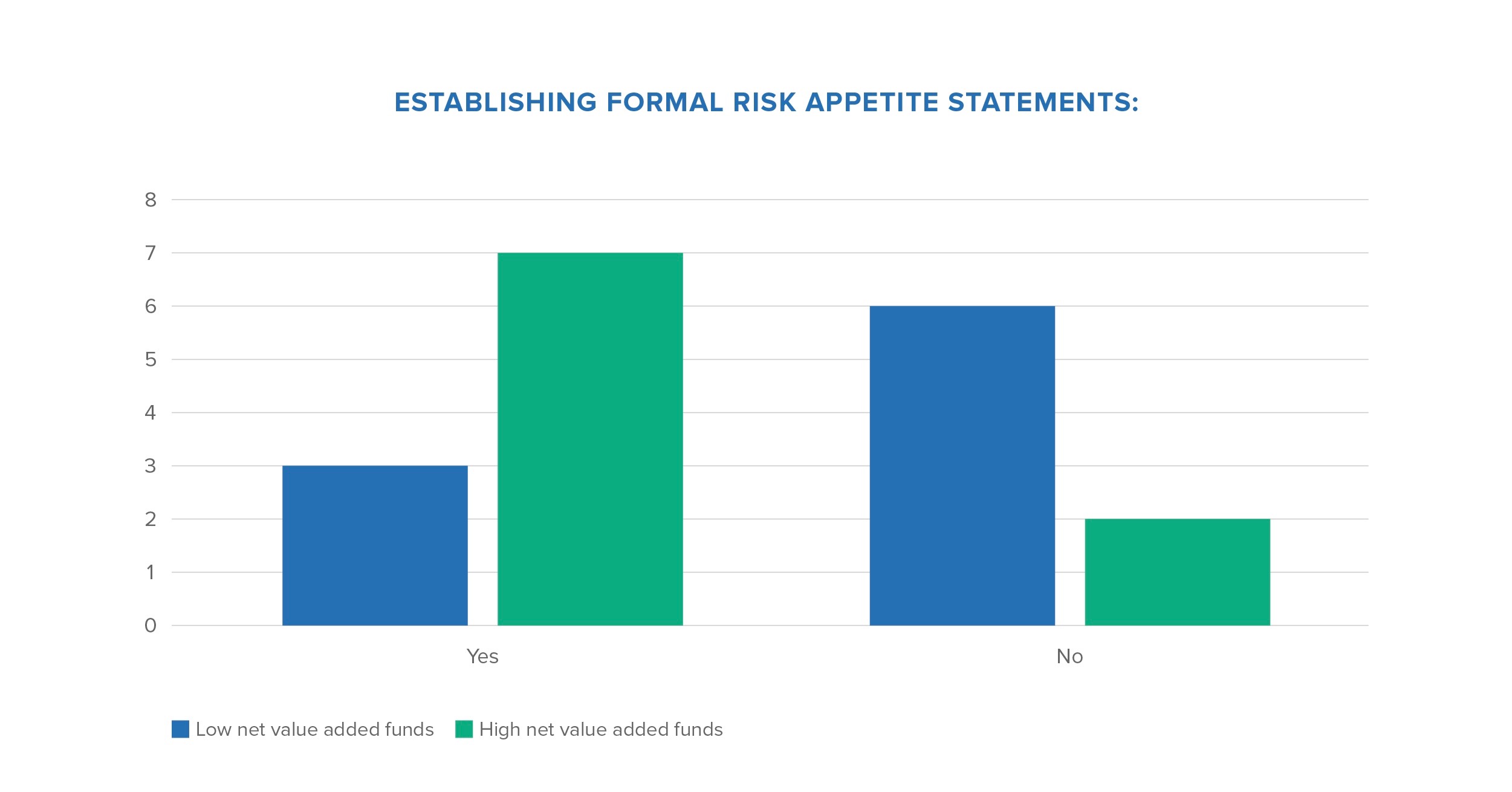

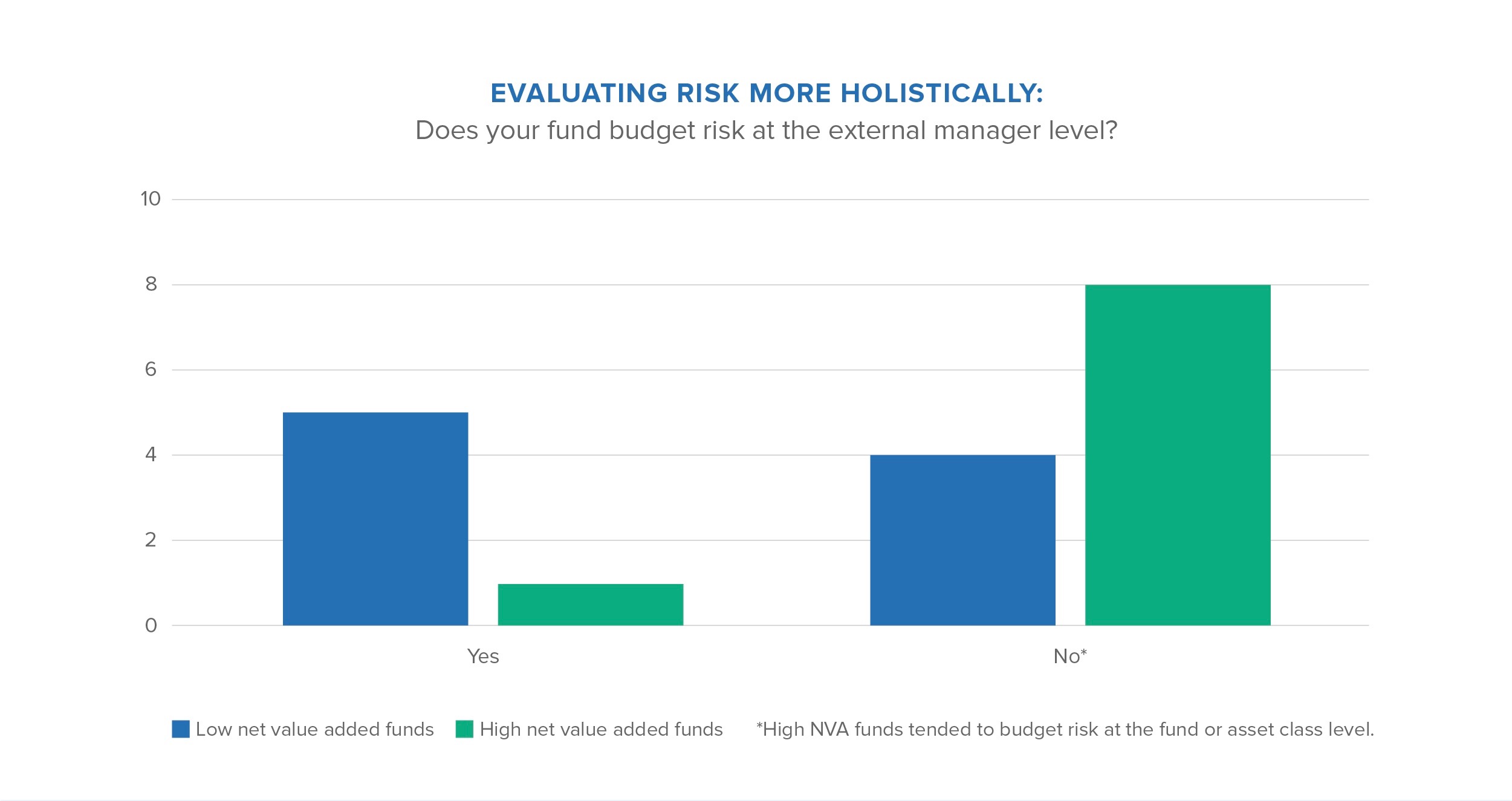

Some other findings are illustrated in the charts below. Asset owners that added net value over ten years further exhibited behaviors which may indicate more stable, long-term stewardship of assets. They had a longer time frame for maintaining investment beliefs, performed self-evaluations of investment boards, had formal statements of risk appetite and analyzed risk at the portfolio level rather than at the individual strategy level.

A substantial body of assets – $1.6 trillion – is being managed by the owners that responded to this survey. The practices of an asset pool this large are noteworthy, but they do not generalize to the whole industry because of the small sample size of 18 owners.

Rather than generalizing to describe the full population of asset owners, these few findings from our survey provide perspective on what is possible and what is worth considering. It is possible for net-outflow funds to outperform over ten years, net of fees, relative to their own policy portfolios. Asset owners may benefit from prioritizing strategy and capital allocation topics in dialogues with corporations. They may also want to consider the stability of their investment beliefs, their use of risk appetite statements, how holistically they evaluate risk, and whether their boards go through the process of formal self-evaluation.

FCLTGlobal plans to explore these areas through several upcoming research projects and is in the early stages of development for a tool that will measure the asset owner community’s progress toward a goal of a collective longer-term focus. Our respondents and partners at CEM Benchmarking helped us to begin that exploration, pointing us in directions that will hopefully yield additional insights into the nature of long-term investment practice. FCLTGlobal has much more to learn, and will have much more to say, on the methods that build and maintain long-term value.

Matthew Leatherman is a Research Director at FCLTGlobal. Michael Reid and Janjaap Weeda are Vice President and Analyst at CEM Benchmarking Inc., respectively.

To comment on this, or any of FCLTGlobal’s current or upcoming research, please feel free to contact our team directly. To receive FCLTGlobal updates, subscribe to our quarterly newsletters and follow along on social media at @FCLTGlobal.