Recent, real-world cases illustrate how external expectations can shape and alter investors’ responsibilities

Recent, real-world cases illustrate how external expectations can shape and alter investors’ responsibilities

Asset owners, asset managers, and companies created FCLTGlobal to encourage a longer-term focus in business and investment decision-making across the investment value chain. Investors around the world agree that navigating emerging responsibilities is an essential component of long-term decision making. Such responsibilities extend beyond an investor’s fiduciary duty or stewardship requirements and are evolving rapidly. They may include the comprehensive well-being of constituents, the entity’s license to operate, or the health of markets, society, or the planet.

Recent, real-world cases illustrate how external expectations can shape and alter those responsibilities. Investors offered a number of examples in the session that FCLTGlobal recently led at ICPM’s Fall Forum, and Schroders recently shared another such case specifically about responsibilities when it reaches an impasse in engagement with portfolio companies.

Our research, including The Long-Term Habits of a Highly Effective Corporate Board and Driving the Conversation: Long-Term Roadmaps for Long-Term Success, repeatedly shows that constructive dialogue between companies and their investors is an important long-term behavior, and impasses are challenging because they may result in an exit, which ends these dialogues by definition. Still, Schroders understands that divestment may sometimes be its responsibility, and is prepared to do so as a last resort.

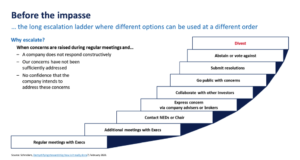

The determination about whether impasse has been reached is quite nuanced for Schroders. Schroders believes that it has a responsibility to exhaust all engagement options before determining that dialogue with a company is at an impasse. An escalation ladder with eight different steps is available to the firm, ranging from regular meetings with management to voting against management on proxy ballot items or proposing a shareholder resolution.

Not every case warrants following all of the steps in order. The order of the steps and what steps are used depends on a company’s unique situation, the nature of the issue, and Schroders’ existing relationship with the company. It marks an impasse only after exhausting all options and still observing that the company has not addressed its concerns sufficiently, does not intend to, and is not responding constructively.

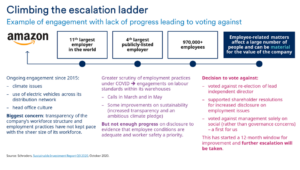

Amazon provides a recent example where Schroders has escalated its engagement with a corporate. In this case, the main concern was that transparency of the company’s workforce structure and employment practices have not kept pace with the size of its workforce. After five years of dialogue and slow progress, Schroders escalated its concerns to a vote against the company’s Lead Independent Director. Engagement is ongoing and further escalation steps may be taken in the future.

Schroders is very clear about the responsibility that it has as an investor once it reaches full impasse in its engagement with a company. “Activism (i.e., getting an influencing stake at the company) is seldom an option, so a true impasse means only one thing: exit.” Still, it is important to note that a “100% exit” happens rarely. Usually, an issue gets resolved somewhere along the many steps on the escalation ladder. Or sometimes an exit may happen on a smaller scale by decreasing investment and, thus, exposure to a company.

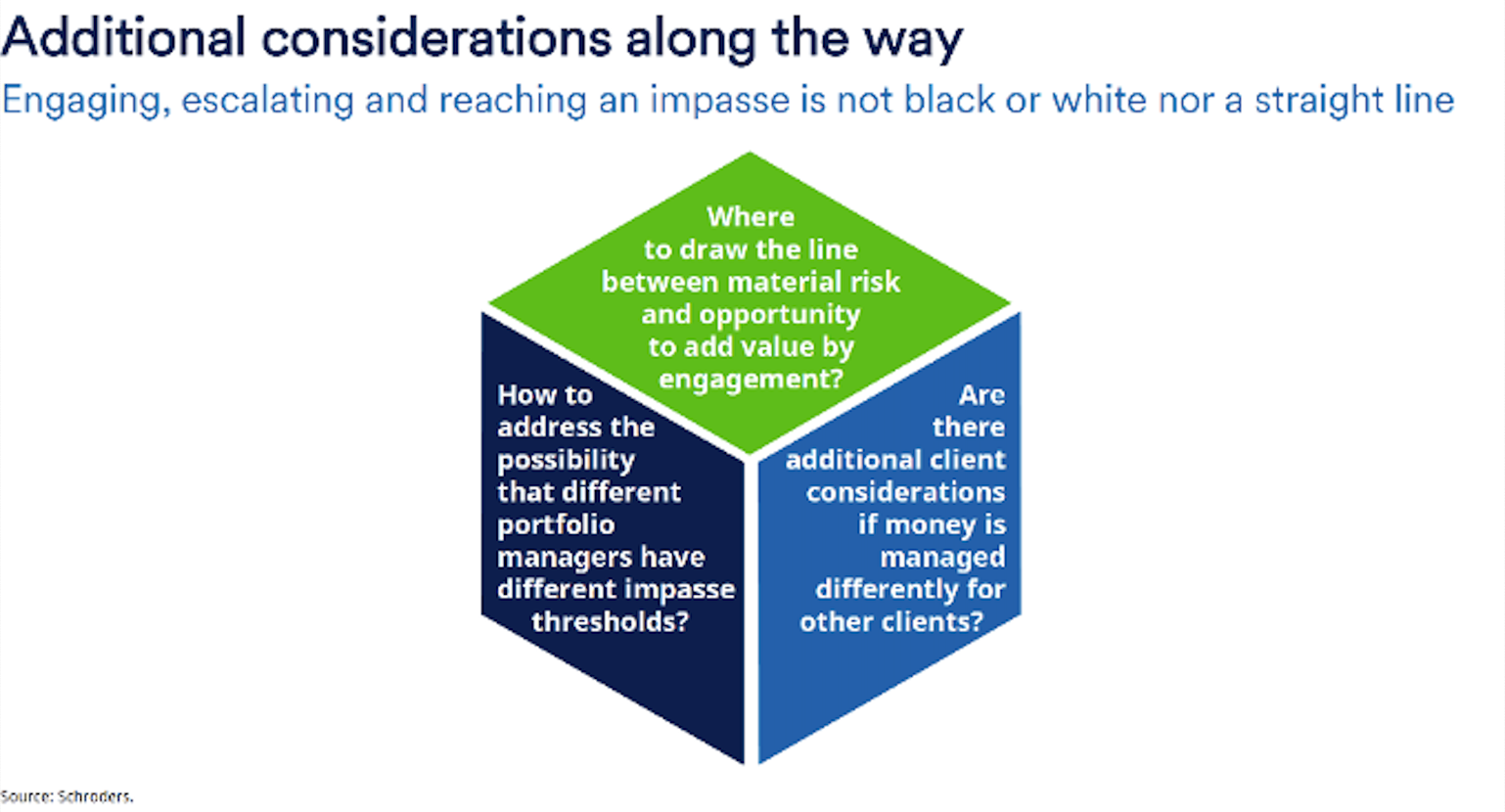

Portfolio managers lead corporate engagements for Schroders, and this can present circumstances in which different portfolio managers have different thresholds of what type of issue poses material risk depending on their portfolios’ investment strategies.

The firm has to balance different parameters as well as considerations of its clients. One way in which Schroders can decrease investment exposure in the course of an engagement is if some, but not all, of its portfolio managers choose to divest based on the type of investment strategy that they manage.

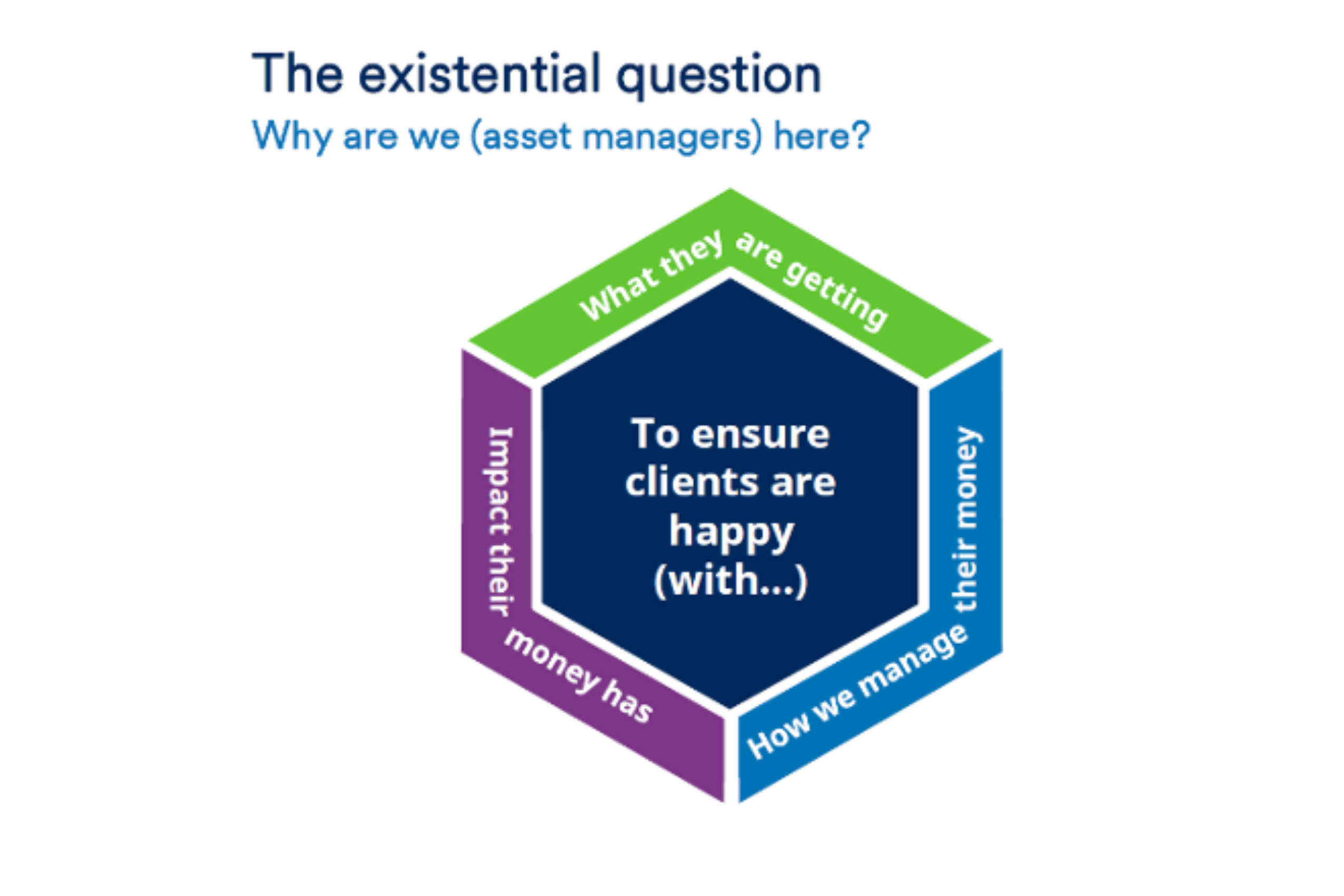

The responsibilities that Schroders feels when it reaches impasses in corporate engagement reflect its purpose, including (among many other dimensions) being an active asset manager of active strategies. This central role of organizational purpose is common for investors evaluating their responsibilities. In Schroders’ language, this involves not just what profits companies generate, but how they deliver those results, and what impact investments have along the way.

Sarah Williamson, FCLTGlobal’s CEO, commented, “We have learned that responsibilities are individual to each investment organization, but it appears that long-term investors face similar challenges in making these decisions. Clarifying and operationalizing this process more widely is a promising area of research about how to focus capital on the long term.” Schroders’ case study about its responsibilities as an investor at impasse during corporate engagement validates this finding, and FCLTGlobal is grateful for this chance to share Schroders’ case because it advances our development of a practical roadmap for investors to evaluate and operationalize emerging responsibilities.

We welcome your input into FCLTGlobal’s broader, ongoing project on investors’ rights and responsibilities. For questions or suggestions, please contact Research Director Matt Leatherman at [email protected].

Investor-Corporate Engagement | Toolkit

25 June 2018 - Strategic engagement is a powerful way for investors and companies to better understand one another and drive long-term value creation.

Article

23 July 2018 - FCLTGlobal discussed private equity last month in London, where CEO Sarah Williamson joined a panel hosted by Schroders, led by Gavin Ralston, Head of Thought Leadership and Official Institutions.

Investor-Corporate Engagement | Report

21 February 2019 - Roadmaps have a proven record at leading companies, and evidence suggests that the majority of investors (especially long-term investors) prefer this approach. By focusing on key elements of performance such as competitive advantages, long-term objectives, and a strategic plan matched with clear capital allocation priorities, companies can build buy-in among long-term investors who support a focus on long-term value creation. Survey after survey indicates that investors prefer forward-looking, long-term guidance around a company’s strategy and expected performance. This paper, which represents the collective effort and experience...