It’s trendy to bemoan the fact that a third of Americans don’t have enough slack in their monthly budget to cover a surprise $400 expense. What about investment institutions in an equivalent scenario?

It’s trendy to bemoan the fact that a third of Americans don’t have enough slack in their monthly budget to cover a surprise $400 expense. What about investment institutions in an equivalent scenario?

We have seen markets roil and institutions totter twice in the past six months over nothing greater than a temporary divergence between bonds’ trading prices and value at maturity. First was the gilt crisis for some pension investors in the U.K., and then west-coast private equity investors ran their own banks.

These institutions have had no slack because they have been positioned for efficiency – an article of faith for us in the financial profession. Anything less, in our parlance, would be suboptimal, value-destroying, imprudent, and potentially even a breach of trust.

The behavior we lament in individuals is the same for which we strive in institutions.1 It’s easier to see the challenge at the individual level – it’s familiar and we can relate with the mentality of “expect the unexpected.” Institutions aren’t quite as relatable but all of these insights still apply, as seen in illustrative examples from Balancing Act: Managing Investment Risk across Multiple Time Horizons.

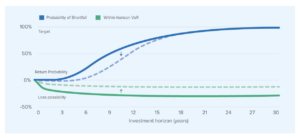

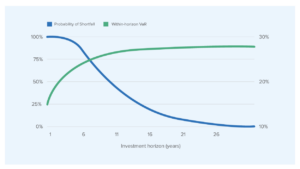

An investor that needs possibility of loss during an investment will need to wait longer to have confidence about hitting their target.

Effect in terms of End-of-Horizon Value-at-Risk of having Within-Horizon Value-at-Risk (10-year horizon), both at 95th percentiles.

Bigger surprises become more probable the longer an investor holds a position, as Figure 1 shows, and that means the investor is likely to face steeper paper losses at some point, including the costs those losses create, like margin calls. 2 This is the institutional equivalent of a surprise $400 expense.

Resilient institutions will have the slack somewhere in their allocations to meet the expense without getting knocked off their strategies. Maximally efficient institutions have no such slack, by design, and covering this surprise cost will disrupt their strategies. It’s clear which of these two is the longer-term institution. It’s the one that can navigate uncertainty and not just foreseeable risks, rather than the fully efficient version that’s vulnerable to any surprise.

Figuring out what it will take to act on these insights at scale is incredibly hard. Generations of received wisdom, coupled with a big first-movers’ disadvantage, have entrenched institutional investors and their leaders into an efficiency-first way of thinking that compromises long-term resilience. But the facts are plain: investors with long holding periods either will do what it takes to be resilient, or they will get disrupted by the proverbial $400 surprise.

Note that it is much easier for an institution than an individual to pass this test. Individuals must have the money before they can set it aside, whereas the only reason the institution exists is because it has the money.

Probability figures and rates-of-change represented in these graphs are based on an illustrative, hypothetical portfolio and will vary materially for real-world portfolios.

Investor Risk and Responsibilities | Article

27 March 2023 - “Do we mean to hold businesses or paper?” The question is one of the most compelling to emerge from Davos this year because its implications are so provocative for long-term institutions.

Article

23 March 2023 - Data about asset-price movements and relationships from the 1990s to today may not represent those that we will experience from today to the 2050s.

Investor Risk and Responsibilities | Article

30 March 2021 - On March 24th, 2021, FCLTGlobal led a risk focus group alongside Alison Taylor and Brian Harward, a team of behavioral scientists from Ethical Systems, an in-house think tank at NYU’s Stern School of Business. The conversation brought together subject matter experts and decision makers with the aim of both understanding why long-term investors default to short-term measurement methods and identifying barriers that prevent them from better aligning risk with their investment horizons.