Corporate R&D spending increased significantly during the pandemic, setting the stage for a future boom in innovation and value creation. Is this a sign of the winners just pulling ahead of the rest?

Corporate R&D spending increased significantly during the pandemic, setting the stage for a future boom in innovation and value creation. Is this a sign of the winners just pulling ahead of the rest?

By Joel Paula

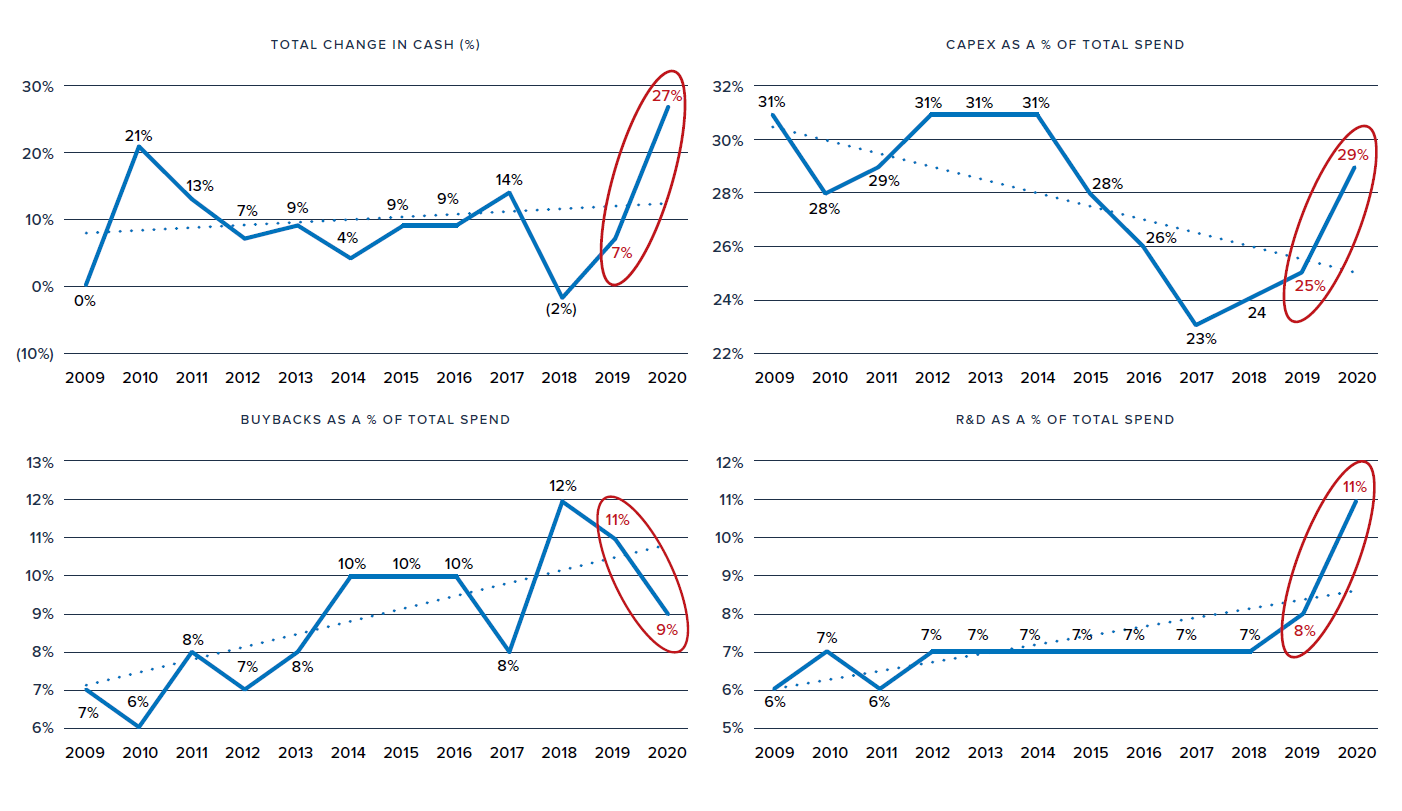

Faced with the need to shore up near-term preparedness and resilience during last year’s disruptions, companies demonstrated a strong commitment to long-term strategy to get through the pandemic. New data from the upcoming FCLTCompass 2021 shows that corporate investment in R&D jumped to levels not seen in the past two decades – 10.9 percent of total spending. And that spending was broad-based across industries, not just driven by the healthcare and pharmaceutical industries racing to treat patients and develop COVID-19 vaccines.

Similarly, investment in fixed assets (capital expenditures) climbed to 29 percent of total spending as companies brought their supply chains in-house and enhanced mission-critical infrastructure. This fixed investment too was widespread and not concentrated in any one particular industry or geography. Potentially due to monetary and fiscal stimulus, data also show that companies had more cash on hand, and that they spent less of it on share buybacks. The broad picture is that corporate cash was put to productive use, setting the stage for a future boom in innovation and value creation.

Percentage of Total Spend, 2009-2020

This is good news born of a year full of bad. It means that, for firms investing in long-term strategies for the recovery, they will be better positioned going forward to benefit from accelerating trends like online shopping, improving sustainability, or decarbonizing business activities.

Studies by professor Hendrik Bessembinder, from Arizona State University, show that investing in R&D, while still achieving superior growth in returns, scale, and profitability is a key characteristic of winning companies. The best-performing 4 percent of listed companies account for the entire outperformance and gain of the stock market since 1926. By analyzing the returns of 26,285 companies, Bessembinder finds that there are four stand-out characteristics that drive success (as summarized in the article published by Baillie Gifford) – all of which are corroborated by FCLTCompass data:

Even though the data in the upcoming edition of FCLTCompass finds long-term investment happening in all sectors (Bessembinder also finds winners in all sectors, not just in technology stocks), market participants are probably wondering how long big tech will continue to dominate. FAANG stocks have powered returns for investors, ballooning from 4.5 percent of the capitalization of the S&P 500 at the end of 2010 to 18.0 percent by the end of 2020. Tesla has been pouring money into research and ramping up production, itself recently topping US$1T in market capitalization. Business activities of the largest tech firms are attracting increased scrutiny from regulators in North America and Europe, particularly on antitrust issues or how digital services should be taxed. China’s clampdown on big tech firms like Alibaba and Tencent has wiped away billions in stock market values. Despite these hiccups, a broad-based shift in long-term investment across markets by many firms is good news for investors who are nervous about big tech and willing to commit to long-term investment horizons.

But what is also clear is that not all businesses have emerged from the pandemic as winners, and some parts of the economy were hard hit and are struggling to recover, particularly small- and medium-sized enterprises (SMEs). Listed firms boast superior access to capital compared to unlisted firms and SMEs, and were arguably better positioned to adapt to challenges posed during the pandemic. The gap between winners and losers has widened as a result.

While a challenging prospect, the data tells us that companies that allocated their capital behind long-term strategies during the pandemic-induced downturn will find themselves poised to capitalize on growing trends in the years ahead, especially as firms set targets and ramp up climate and sustainability investments.

18 December 2024 - FCLT Compass is a dashboard measuring the investment horizons of the global investment value chain, how households are saving and allocating their money, and how long they can live off those savings. Calculating these metrics provides a holistic understanding of the long- or short-term orientation of global capital markets and how that orientation impacts the financial futures of millions of people worldwide.

Innovation | Toolkit

9 August 2020 - An interactive R&D Scenario Engine that allows corporate boards, executives, and risk committees to determine their optimal R&D allocation between short, mid, and long-range projects.

Article

11 January 2021 - By Allen He As noted in Funding the Future: Investing in Long-Horizon Innovation, it can sometimes be shrewd for investors to consider their portfolio companies’ research and development (R&D) pipelines as a series of options. Doing so can provide an alternative way of valuing a company and may help reveal a differentiated view of a company’s potential upside from R&D investment. R&D pipelines share several similarities with call options, chief among them their value pertaining to volatility and time to maturity. A chronic problem discussed in Funding...